In response to a comment, I'm posting here because I was limited to 4096 characters there.

Great question. Sorry for the long answer. I hope you read it.

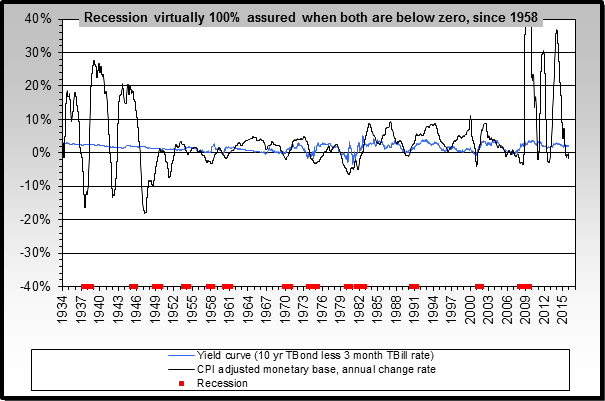

In response to the economy being on the mend, I doubt it. ECRI has still not rescinded their US recession call. However, one of the charts I link to on my page still doesn't say "recession"as the CPI adjusted monetary base has been permanently elevated, and the yield curve hasn't inverted. I will try to create a Shadowstats adjusted CPI deflated Monetary Base and post it.

http://www.nowandfutures.com/images/predict_recession2.png

I usually don't try to figure out why because usually the "whys" might get in the way of rational thought. This time the reason why would have definitely helped with my conviction.

For whatever reason - maybe Christmas shopping, I completely missed the LTRO announcement or failed to understand it right away as I was being white washed with all the other alphabet soup acronyms out of the Eurozone that all seemed impotent at the time. The LTRO announcement came within a few weeks of the bottom for gold, silver, oil and stocks. As I understand it, the benefit here is it allowed banks to get fresh liquidity for up to 3 years in exchange for assets rated A or better. This allowed them to get some stuff off their books, use the fresh liquidity to buy sovereign debt, and the ECB to massively expand their balance sheet.

http://www.ecb.int/press/pr/date/2011/html/pr111208_1.en.html

Beyond that fundamental reason, I posted these two posts around that time.

http://thelastcanary.blogspot.com/2011/12/21-dec-2011.html

http://thelastcanary.blogspot.com/2011/12/19-dec-2011.html

They alluded to possible bottoms because we were oversold from a technical standpoint, but not with much conviction unfortunately for readers. I went long around that time most of the leading stocks, and did not get much out of them when I exited in mid January.

I always forget it, but I have a theory that the end of rallies really pick up the steam for weak stocks. You can see this in the 07 / 08 rallies too. As you can see the McClellan index actually bottomed in August, October and December with each low higher than the last.

The best stuff bottomed in August and outperformed since then. However, as those prices went up, the expected rate of return from them goes down, and they look more and more scary as they take out new highs.

Therefore, the "left out" assets become more enticing on a relative basis. Basic sector rotation occurs squeezing the easy performance out of the best, then the middle, and then the worst in the three (there aren't always exactly three) cycles.

As a quick example, see the following IBD favorites

:http://stockcharts.com/h-sc/ui?s=PII&p=D&yr=1&mn=0&dy=0&id=p69326070535

http://stockcharts.com/h-sc/ui?s=BIIB&p=D&yr=1&mn=0&dy=0&id=p56168368637

http://stockcharts.com/h-sc/ui?s=ALXN&p=D&yr=1&mn=0&dy=0&id=p73373376395

All have performed very well (20 - 50% up) since their August bottoms. None of them came back near that low.

Therefore, as the top performers rose they no longer appeared to offer "value" for large investors, while the laggards stayed weak - and relatively, their fast performance the past few weeks still hasn't caught them up with the high fliers in terms of performance since August.

http://stockcharts.com/h-sc/ui?s=ING&p=D&yr=1&mn=0&dy=0&id=p89249629446

ING up 10% or so from August bottom.

http://stockcharts.com/h-sc/ui?s=LYG&p=D&yr=1&mn=0&dy=0&id=p32944887514

LYG pretty much flat from August bottom. Truly pathetic despite its strong "catch-up" rally recently.

http://stockcharts.com/h-sc/ui?s=STD&p=D&yr=1&mn=0&dy=0&id=p06042658944

STD down a bit still. Pathetic.

NBG and IRE are both still below their August lows despite large gains the last few weeks.

These weak players are just enjoying the final phase of the rally that started in August. This is their day in the sun and it will end much like it has every other time. XLF as whole is still completely underperforming since August. They will not catch up. Most of these banks are bankrupt and will continually reverse split as they will continually be worth pennies. Their models (lending money to sovereigns that can't pay or citizens that can't pay doesn't work well) can no longer generate organic growth. Any money they get is just created and therefore does not represent real value or growth.

And vice versa, the same applies, a bear market is not over until it claims the strongest performers. Right now, it has really only gripped the weakest and let them come up for air recently.

http://stockcharts.com/h-sc/ui?s=$USHL5&p=D&yr=3&mn=0&dy=0&id=p07931405274

As you can see, it has slowly been claiming leaders as we still have quite a few less new highs than we did in 2010 and 2009 despite the latest moonshot.

{kind=link}

Scott,

ReplyDeleteThanks for your detailed answer. I think you are right about the LTRO. I believe that Bill Gross has described the LTRO program as "backdoor QE". It has stabilized Europe for the time being. I believe another round of LTRO is planned for February 29.

You may also be right that the crummiest stocks are the last ones to join the recent 4 month rally that started in early October when it seemed that all was lost.

Thanks again for posting your blog. I am always learning something new.